Earlier this month, CMS announced the first cohort of Next Generation ACO (“NGACO”) providers (see here our summary of the key changes made in the Next Generation). Below are a few thoughts on who signed up:

The Next Generation cohort is diverse

The cohort of 21 participants has the flavor of a structured pilot:

- Heritage mix: 8 are former Pioneer ACOs (with 232K lives attributed in 2014), 8 came out of former MSSP ACOs (217K lives attributed in 2014) and 5 are new to the CMS ACO program but with some experience in commercial ACO arrangements

- Size mix: Some are building off of relatively small programs (e.g. Iowa Health / Trinity Pioneer with 9K; Cornerstone MSSP in North Carolina with 17K) while others are quite large (e.g. Pioneer Valley MSSP with 36K and Steward Pioneer with 63K)

- Market mix: Some are in urban environments with significant branded competition (e.g. Steward in Boston, Henry Ford in Detroit, the Los Angeles-based ACO players), while others are rural (e.g. Beacon Health in Maine) and have strong market positions (e.g. Deaconess Health with a 60%+ share or Triad with a 60-70% market share)

Evidently, Next Generation’s appeal is broad (and it is not just engineered to solve Pioneer problems) and the program’s changes have attracted some “fresh blood” – great news given CMS’s goals to expand risk contracting. CMS said they expected 15-20 systems in the first cohort and in fact got 21 (it would have been 20 had Bellin and Thedacare not decided to split into two ACOs. The two systems collaborated as a single Pioneer ACO), suggesting that there may have been more applicants than slots and an opportunity for CMS to actively design the cohort to ensure the broadest set of learnings.

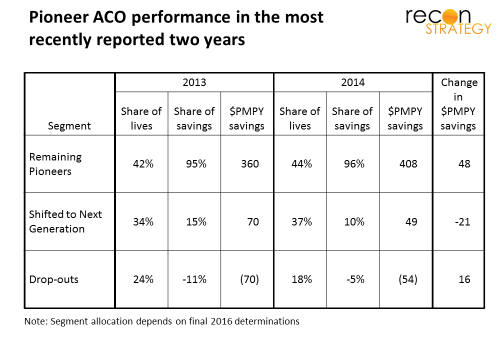

Former Pioneer ACOs tended to be weak performers looking for program “fixes”

In general, the Pioneer ACOs which signed up for Next Generation were treading water over past couple years (top performers which together made 95% of the total savings of the program are sticking with Pioneer, the ones with major losses have departed). The average savings achieved by the eight ACOs fell from $70 to $49 PMPY between 2013 and 2014 (a 30% decline), while the 9 remaining Pioneers saw their savings vs. benchmark rise from $360 to $408 over the same time frame (a 13% increase).

Presumably the adjustments to Next Generation will help these systems get their ACOs back on track — though which changes are most important may vary by provider. For example: Beacon Health in Maine has argued that they are penalized by Pioneer for being the low cost provider and was probably attracted by adjustments for relative regional and national efficiency built into the Next Generation benchmark. On the other hand, Steward competes vs. nearby strongly branded systems (e.g. Partners) and may have been attracted by the Next Generation’s member engagement tools (e.g. reward for staying in network), benefit enhancements and options to develop risk contracts with preferred providers.

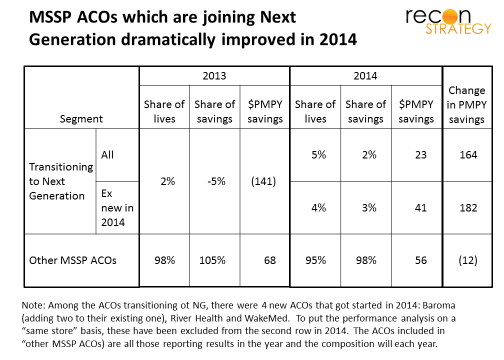

Former MSSP ACOs have “figured it out” and are ready for the “next level”

The eight NGACOs with roots in the MSSP program started off badly in 2013 (with attributed beneficiary costs exceeding targets by an average $141 PMPY), but dramatically improved in 2014 – tripling attributed members and improving average savings by $180 PMPY (to $40 PMPY savings level – excludes several MSSP ACOs which launched in 2014). By comparison, the other MSSPs not transitioning to Next Generation held roughly steady over 2013 and 2014 with average savings of $68 PMPY in 2013 and $56 PMPY in 2014.

The Accountable Care Coalition of Texas, for example, saved $566 PMPY vs. target in 2013 and $734 in 2014 (and presumably the South East Texas portion of that coalition that signed up for the Next Generation program had equally strong results). Making the shift to Next Generation for this ACO should allow two key benefits: (1) access to a larger share of the savings they are generating than is available under MSSP and (2) an ability to exploit the competitive cost position over past couple years by shifting to a benchmark which rewards efficiency vs. other providers (not just vs. own past performance).

Not all MSSPs have it so good: Triad Healthcare in North Carolina saw their PMPY savings decline from $525 in 2013 to $100 in 2014, while Deaconess Care in Indiana saw costs consistently about $600 PMPY above target. Recall these two systems are leaders in their markets. One can imagine an ugly adverse selection scenario in such systems where patients who become ill shift their care to the leading system in the region. Disease risk adjustment would provide no relief because, under MSSP, it can only lower, not raise the benchmark. Further, because members are attributed retrospectively, the provider systems would have only limited ability to bring their care management infrastructure to bear. Both issues are addressed in the Next Generation model.

Next Generation unlikely to be the final generation

There are a couple reasons why the model will be a stepping stone and subject to more changes:

- Five participants are new to Medicare ACO. While they bring experience from commercial risk contracting and health plan management (e.g. Henry Ford), they are also likely to identify fresh problems with the overall ACO model which CMS will want to fix (in order to keep attracting new systems to the model)

- Some ACO features are being tested at scale for the first time (member engagement, benefit enhancements and preferred provider risk contracting) and were likely critical to getting some providers (e.g. those with nearby branded competition) to join. It will likely take a cycle of learning and tweaks to figure out how to make these really effective (for example, I think we will quickly learn that a $50 bonus to members for staying in the ACO network is too small to counter the attraction of big AMC brands).

If the relatively small size of the Next Generation cohort (450K participants among the known ACOs) and high degree of cannibalization from existing ACO programs (16 of 21 program participants), Next Generation is unlikely to be more than an incremental modest net contributor to CMS’s ambitious goals for rolling out risk sharing across providers in the next few years. Look to other programs (e.g., bundled payments etc) to do a lot of the work.