This past January, Walgreens assigned operational control of 56 in-store clinics to Advocate Health. The deal signals another intensification of the already fierce hospital competition in Chicago, and may have implications for the future of urgent care broadly.

Prisoner’s dilemma

Healthcare’s market failures often prevent the timely exit of redundant capacity, so any new care capacity ends up raising – rather than reallocating –fixed costs across a market. Urgent care, which is enjoying widespread and rapid growth, can be an exception: many providers lack the scale and geographic concentration of patients to support attractive after-hours care. As a result, a lot of minor acute demand clogs up the EDs — not only adding cost but potentially driving high acuity / higher margin cases to hospital competitors.

Ideally, urgent care should operate as a competitively neutral utility. Minor acute care is highly templated and (to the extent continuity is required) easily integrated into primary care relationships. Mixed in with the daily roster of low acuity care are a handful of complex cases, which urgent care centers refer out. If urgent care supports existing patient-physician relationships and triages out the high acuity cases in an unbiased way, there should be little reason for provider systems to build their own (United’s acquisition of the largest national urgent care chain – MedExpress – is likely premised on reinforcing strategic neutrality vis-a-vis the local major providers in each market).

There is plenty of gross margin in the referrals and urgent care patients are often medically “homeless”. (Published surveys suggest 3-5% to EDs and potential admission, 10% for specialist follow-up and potential procedures, and 10-15% for more sophisticated diagnostics. Do the math with simple assumptions and this referred out care could be worth as much as $50 in provider gross margin for every urgent care patient – even if concentrated in just a few). If an urgent care center starts steering patients towards one system, the provider systems are going to feel it. If a critical mass of urgent care abandons strategic neutrality, provider systems will be forced to set up their own urgent care networks in self-defense.

The likely result: lots of duplicative capacity and centers using referral profits to operate well below break-even. If each system builds an urgent care network commensurate with their overall market share, the net effect on patient allocation will be minimal — but plenty of capital will be wasted on redundant facilities.

Land grab dynamics

Smaller provider systems have the biggest potential for gaining share from an owned urgent care network, so it would seem logical to expect them to “defect” first. But what if the market is already saturated with independent urgent care?

A given market produces only so many urgent care episodes (about 1 episode for every 2 people) limiting the number of viable centers. Right now, Chicago has one urgent care center for every 60-70K people – beginning to approach “rules of thumb” saturation levels. Further, location is critical for urgent care and there are a paucity of good sites. We have, in effect, a musical chairs scenario: once the defections start, the slowest providers are going to be left with poor site options – or none at all. Under these conditions, it can make sense for larger, well-resourced players to make the first move to capture the best sites and chains before the other providers “wake up” and bidding wars start.

Hospital control over a critical mass of well-situated urgent care can also provide leverage against plan narrow network strategies. Plans will be reluctant to carve out urgent care centers because they are so much cheaper than the ED. However, if the plan keeps hospital-owned urgent care in but carves the owning hospital system out, members using these centers may be reminded of network restrictions every time they get a referral. Plans may be willing to accept somewhat more generous terms to avoid that kind of member dissatisfaction.

The Chicago way

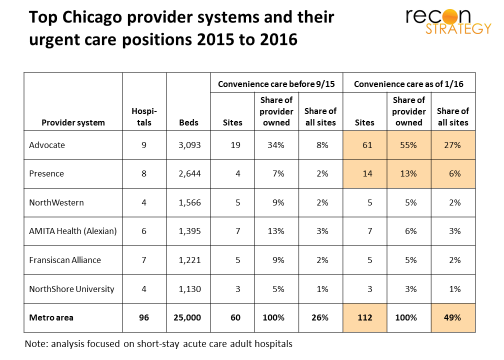

Chicago offers an illustration for these urgent care defection dynamics. There are about 225-230 convenience care sites in metro Chicago, 60 of which (26%) were owned by a provider system as last summer. (Folding in CVS and Walgreens retail clinics into this category given the large overlap in scope of care, location convenience and hours available in these models as in urgent care.) That is not necessarily a tipping point. Many hospitals own a few urgent care centers to declutter their EDs and some provider groups have pockets of sufficiently concentrated patients to support an urgent care / clinic combination. Neither should threaten an urgent care equilibrium. Chicago’s largest provider system (Advocate Health) has the largest share of urgent care among providers but was a mid-sized urgent care player in a fairly fragmented market (8% of all sites).

In September 2015, Presence grabbed 10 Chicago urgent care sites (through a joint venture with Physicians Immediate Care), allowing them to get closer to Advocate (14 vs. 19 sites for Advocate at the time). Then, this past January, Walgreens handed over control of their Chicago clinic operations to Advocate, contributing 56 sites (42 in Chicago metro) and giving Advocate 27% of all convenience care sites in the market. Now, about half of all convenience care sites are affiliated with a provider system.

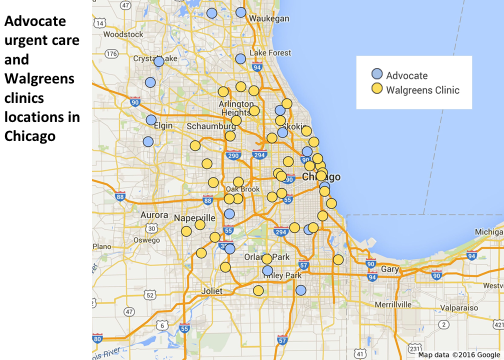

The Walgreens sites add density to Advocate’s existing network but also provide access to whole new neighborhoods such as Arlington Heights, Schaumburg (Alexian Brothers), the West Side (which several independent hospitals serve), downtown (Northwestern), and the south (University of Chicago and Franciscan).

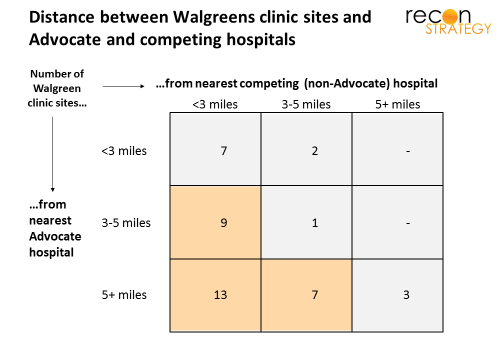

Walgreens has indicated that “the clinics will function in the same manner as they have been thus far when Advocate takes over”. But the pressures to steer – however softly – patients to the Advocate mothership will be hard to resist. In the exhibit below, we’ve mapped each Walgreens clinic to the nearest Advocate and nearest competing (non-Advocate) hospital. Twenty-nine (of the 42) are closer to competitors than to Advocate and thirteen are more than 5 miles from an Advocate hospital but less than 3 miles from the nearest competing hospital – in other words, deep in competitor territory.

The result is not surprising (assuming that Walgreens did not try to locate the clinics near Advocate hospitals when they were originally launched) given that Advocate has only 9 of the 96 short-stay acute hospitals in the Chicago MSA, But that fact will provide cold comfort to Advocate competitors. We did a similar analysis putting Advocate and North Shore together just in case the Walgreens deal was hatched with the prospective merger in mind and the pattern was very much the same. Walgreens locations further from Advocate and North Shore sites than competing hospitals.

Advocate’s play does not leave a lot of obvious options for other systems. There are about 35 independent urgent care sites, a few of which could be part of a hospital’s defensive perimeter. Concentra – in some strategic limbo after its recent departure from Humana — might be available for an alliance. The other sites have homes in large and strategically committed parents (MinuteClinic with CVS, MedSpring with Fresenius), so the pickings are slim. Given 220+ existing sites, green field will be hard to find and have a limited role at best.

Whither convenience care?

There are two sides to every deal. What led Walgreens to sell?

New leadership at Walgreens had certainly signaled a more conservative approach to clinics (closing some, laying off nurses, trimming hours, etc). Chicago may have been a particularly challenging market to get volume given the looming saturation of urgent care. Walgreens did a similar deal with Providence Health in the Pacific Northwest which are already saturated. Also, Walgreens has been using a proprietary EHR but recently announced plans to roll out Epic. Epic’s price tag has driven many hospitals to seek partnerships. Part of the Walgreens/Advocate deal is installing Epic in the included sites. Finally, after the Theranos debacle, perhaps they have lost some confidence in their ability to maintain a strong clinical brand (as distinct from a pharmacy brand).

The Advocate and Providence deals may also reflect Walgreens’ evaluation of an emerging challenge for convenience care generally coming from telehealth. Although telehealth is largely focused on the same minor acute cases as urgent care, its impact has been minimal because we are early in the adoption curve (the percentage of employers offering telehealth was in the teens just a few years ago, and, even today, utilization is usually measured in basis points). But that is changing with growing familiarity. More minor acute patients taking up smart phones and tablets means shrinking volumes in urgent care waiting rooms. Urgent care will need to move up the acuity ladder to treat more complex patients to protect their economics — putting them at odds with local providers unless they are working in partnership.

Walgreens began experimenting with telehealth (MD Live) in 2014 and is rolling out to 25 states. Washington state and Illinois were in the second wave of roll-out. These pilots may have persuaded Walgreens that telehealth poses serious risks to convenience care sites in the absence of partnerships around higher acuity care. Perhaps the game of musical chairs is reversed: it is not which provider systems acquire the best urgent care centers but which urgent car e centers form ties with best provider partners. If so, Walgreens has bagged itself the biggest player in town.

Implications

- While urgent care’s strategic neutrality may be right for the system as a whole, intense provider competition and market saturation makes it hard to preserve

- The Advocate deal confirms Providence was not just a one off and that Walgreens is serious about selling its clinics, not just selectively rationalizing. If you are in a markets with a lot of Walgreen clinics, start running the scenarios

- Leading provider systems may see owning a critical mass of urgent care as a leverage against payer network strategies; pushing telehealth alternative may be the payer’s best response