Who will be the first to take integrated health care delivery national?

A few years ago, the best bet might have been an established provider with a nationally compelling brand and a growing affiliate federation such as Cleveland Clinic or Mayo. Instead, Optum – just a decade ago three separate services largely focused on serving United’s health benefits business – has entered care delivery and — by a constant stream of acquisitions big and small — built up beachheads in a majority of markets and is – via ongoing big acquisitions, tuck-ins and greenfield expansions – laying the foundations of a national integrated ambulatory system.

Particularly in light of the latest rumors about the role of clinics in driving the value of a potential AET-CVS combination, it is timely to take a look at what Optum has put together, size its geographic reach and discuss some strategic implications.

OptumCare’s three-pronged entry into ambulatory care

OptumCare’s delivery consists of three broad components:

- Physician practices owned directly and managed via Optum-owned independent practice associations (IPAs) which provide administration, support services and structure the risk contracting

- Urgent care facilities able to address a material share of care provided by hospital emergency departments at a significantly lower cost

- Ambulatory surgical centers (ASC’s) which can support a growing share of lower acuity surgeries while avoiding the cost of an admission and some of the displeasures of traditional hospital encounters.

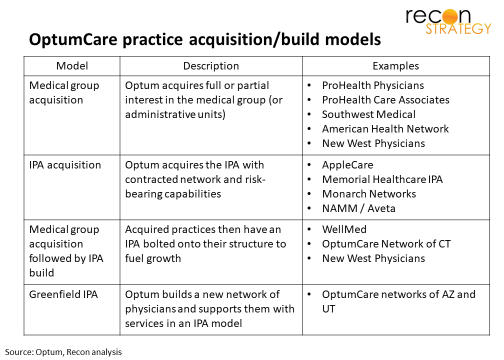

Optum has been active in practice and IPA acquisition since at least 2010 (first major care delivery focused acquisition was AppleCare Medical Group and Memorial Healthcare IPA in Orange County) and has owned practices since at least 2008 (the Las Vegas group Southwest Medical acquired as part of UnitedHealth’s acquisition of Sierra Health). Over time, Optum has built up a large clinical presence via a few avenues:

Acquisitions have been supplemented by investment by organic growth within these practice units (for example, OptumCare of AZ moving into Tucson, WellMed moving into Dallas) or tuck-in acquisitions (e.g. Wellmed buying USMD). At this point, Optum reports having 20K affiliated physicians.

This relatively slow and steady practice acquisition strategy over the last 7 years has been paired with a “big bang” expansion in urgent care and entry into ASCs driven by two major recent acquisitions:

- MedExpress, an urgent care chain with a broad multi-regional presence, acquired in April 2015. At the time, MedExpress had 141 sites open and another 30-40 in the pipeline but Optum has grown the network to 280 sites today

- Surgical Care Affiliates, an ASC center operator with 190 locations run as joint ventures with local physicians or health systems acquired in January 2017.

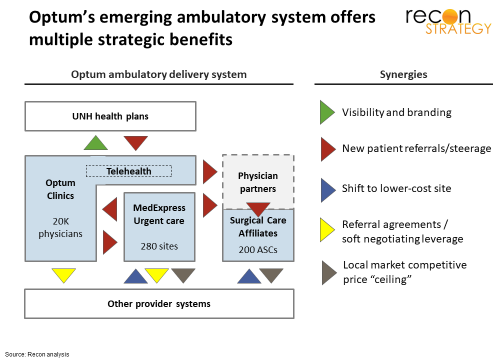

Value of OptumCare

In our view, there are five or so major potential synergies across OptumCare components (to the extent they are operating in the same geography) and between OptumCare and UnitedHealth’s health plan business:

Here’s a quick description of each:

- Visibility and marketing. OptumCare locations can enhance the visibility and awareness of UnitedHealth products. For example, a friend of mine in TX told me about health plan brochures in the office of his primary care provider shortly after the acquisition via WellMed.

- New patient referrals. OptumCare sites can receive prominent positioning in United plan network guides. United can also ensure a favored position for OptumCare in its narrow networks. And, United can perhaps ensure faster access to primary care via Optum in regions where panels are full. Within OptumCare, clinics can send patients to an urgent care for after-hours care and urgent care can send patients without a primary care medical home to an OptumCare practice. Patients needing non-urgent surgical care can be referred to the providers participating in an ASC joint venture.

- Shift to lower cost site. Urgent care is an attractive alternative to emergency departments for lower acuity needs just as ASC’s offer better value than hospital operating rooms for lower acuity surgeries.

- Soft negotiating leverage. Clinics and urgent care sites regularly encounter patients requiring higher levels of care and these can be strategic about where to softly steer those patients. For example, an urgent care center may have a simplified “one call” system to get expedited appointments with specialists which is of value both to the patient (faster access) and to the receiving provider (more volume). Not hard to imagine that a provider system might have an easier chance at getting those referrals if it is a good partner on rates with United

- Local market competitive price “ceiling” Many health systems are building their own urgent care and ambulatory surgical centers. If these health systems try to mitigate the cannibalization by keeping prices on services these settings somewhat higher than warranted, Optum’s local alternative pricing can provide useful leverage for United network negotiators.

Three intriguing aspects to the OptumCare ecosystem:

- Urgent care and ASCs are long-term bets on taking more care out of hospitals. Every time United – or any health insurer – pushes harder transitioning care to these new models, Optum stand to capture an equity windfall.

- In many markets, physicians have decided that maintaining their independence from hospital-based systems is too challenging and become affiliated or acquired. Optum is making a major bet that hospitals are stranded assets in the long-term and that their ambulatory assets can thrive without an organizational linkage to a local hospital as long as United (and its technology and capital) is behind them.

- None of these synergies require that OptumCare offer favorable rates to United or that the ambulatory system acquire share-based leverage vs. United’s competitors in any market. United does better if other payers find OptumCare an attractive provider to have in their networks. As with Amazon business units, the exposure to unaffiliated buyers hedges against the complacency of a secure customer base which afflicts vertical models.

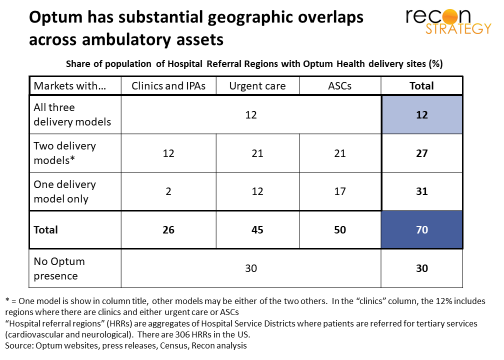

Geographic penetration

As a national insurance player, United will reap more power the more geographies in which OptumCare operates. Given the synergies across components, OptumCare’s impact is stronger if all three components – clinics, urgent care centers and ASC’s – are concentrated in a particular market. This is a classic breadth vs. depth challenge which United has been addressing with the steady acquisition and growth in practices and IPAs coupled with “big bang” acquisitions of geographically dispersed MedExpress and Surgical Care Affiliates chains. How far have they gotten?

We mapped out the clinics identified as part of an Optum acquired practice or IPA, MedExpress or Optum-branded urgent care centers and Surgical Care Affiliates sites (naturally there is some judgement involved in classifying practice and we may not have captured the most recent urgent care center builds or closures). We then identified how many regions had one type of care, two types of care or three types of care and weighted by population and, weighting those regions by population, identified the total share of population with access to OptumCare (we did not weight by number of clinic or urgent care or ASC sites per region). In the exhibit below, we used Hospital Referral Regions which are aggregates of the 3,500 or so Hospital Service Districts where patients are referred for tertiary services as best capturing the opportunity for OptumCare to be working with multiple hospitals.

At this point, we estimate that about 70% of the US population has access to some OptumCare and 12% has access to all three types of OptumCare.

The geographic reach Optum has achieved in seven years is remarkable and, if Optum maintains its recent pace of investing (e.g. buying a 300 physician practice in Carmel Indiana in April 2017 for $184M or doubling the size of the MedExpress urgent care site network since its acquisition in 2015), the platform can quickly become ubiquitous.

Implications

- In our view, it is highly unlikely that Optum will use leverage in local care delivery to UnitedHealth’s direct advantage: United is not seeking to build a Kaiser: the fixed costs of health care delivery – even in ambulatory – are too high to risk losing volume by not contracting with a competing payer and the equity value of capitalizing on the long-term shift towards ambulatory across all payers a are too attractive to not contract with competing payer.

- This doesn’t mean that competing payers should not be wary: as United puts pressure on local delivery systems on surgery rates via its ASC presence, those systems may accept lower rates from United but may seek relief with higher rates from other payers.

- OptumCare’s three major pillars are likely not the final configuration. Optum has been making some efforts in palliative and hospice care. Another interesting avenue would be in stand-alone imaging. RadNet has an interesting model of structuring joint ventured free-standing imaging networks with leading local delivery systems looking to have an option on payer pressure to push imaging out of expensive hospital settings.

- As noted above, rumor is that CVS’s clinical capabilities are a key element of the synergies behind a potential CVS-AET deal. While CVS’s clinical capabilities (especially MinuteClinic) are impressive and certainly have terrific geographic breadth, the actual clinical scope is substantially slimmer than OptumCare. If the AET-CVS merger strategy teams have United in their competitive sight, they would need to do a lot of enhancements to match what United already has.