Closed vs. open

Hospitals can compete for patient referrals either by exclusively affiliating with a subset of physicians (“closed model”) or by collaborating with as many qualified physicians as possible irrespective of competing affiliations (“open model”). (Both of these strategies are from the perspective of the facility, of course. A population health strategy would still focus on affiliating with physicians to aggregate patients, but with a goal of minimizing (not just directing) facilities based care.)

The two strategies are generally incompatible. If most hospitals use the same approach in a market, you can get a kind of competitive equilibrium. But, if there is any mixing, the closed model usually dominates even if not actively chosen. If Hospital A requires exclusive affiliations with critical referral sources while competing Hospital B does nothing, Hospital B will by default find itself working with a de facto exclusive network made up of the physicians left over.

Allowing a competitor to cherry pick among referral sources is not wise, of course. Once Hospital B detects what Hospital A is up to, Hospital B will follow suit (if it has the resources). The result will be an affiliation land grab via practice acquisitions, clinical integration agreements, recruiting new physicians to fill gaps left by competitor coups and expansion of care sites to ease access and grow the funnel for patients.

Capital District case study

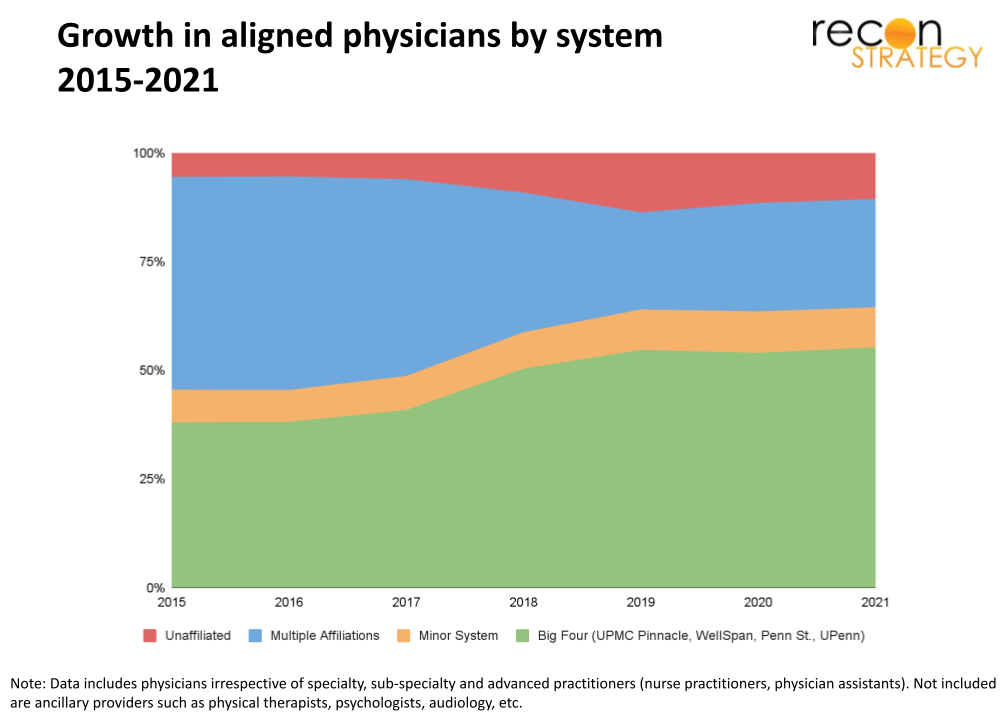

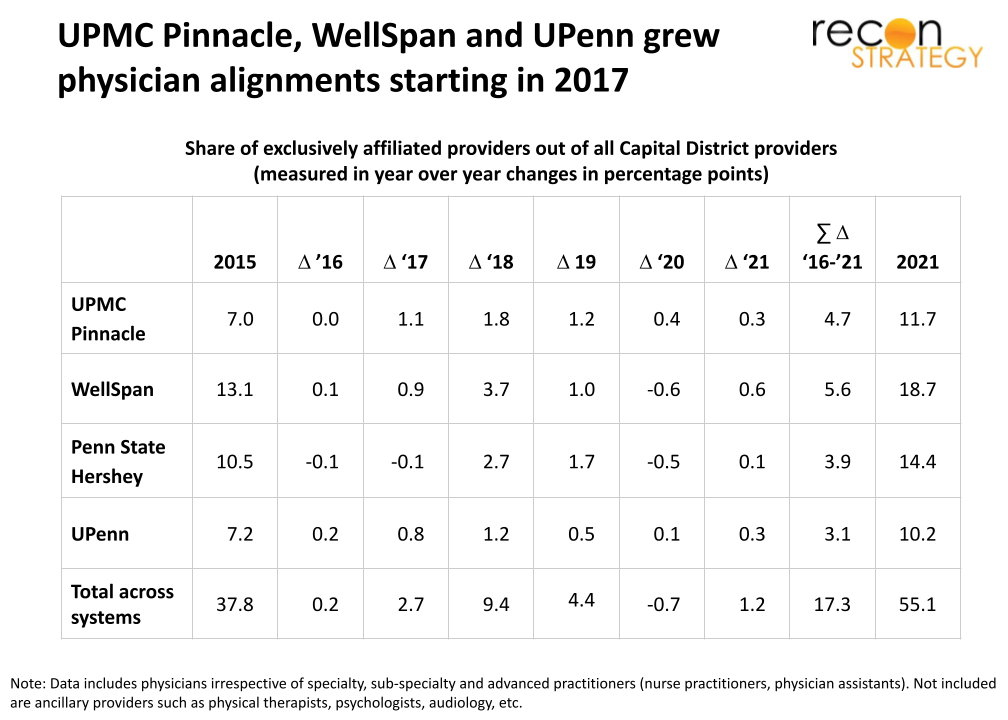

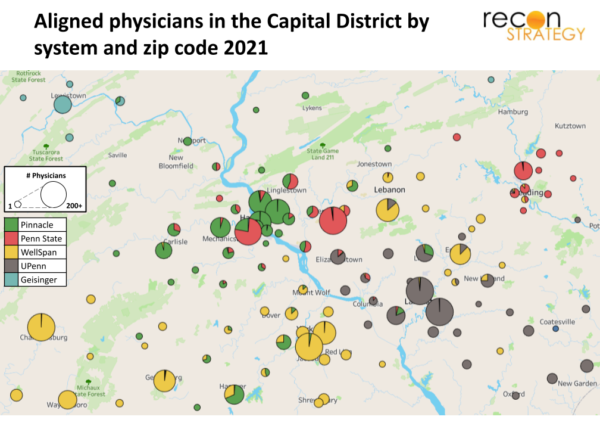

The Capital District in Pennsylvania offers a remarkable case study of this transition.[1] Over the last five years, the share of providers with alignments (which we define as reporting affiliations with hospitals exclusively part of one system[2]) to one of the “Big Four” systems[3] (WellSpan, UPMC Pinnacle, Penn State Hershey and UPenn[4]) went from ~38% to ~55%. This statistic won’t surprise any attentive reader of the Patriot News where reports of new clinic groundbreaking, new doctors and new affiliation and practice name changes have been recently commonplace.

WellSpan, UPMC Pinnacle and UPenn appear to have been the first to start locking in provider alignments (between 2016 and 2017) while Penn State Hershey started about a year later. Our annual snapshot data is not fine-grained enough to determine whether WellSpan, UPMC Pinnacle or UPenn moved first. The data could be consistent with a guess that UPMC’s entry by acquiring Pinnacle disrupted an “open model” equilibrium. UPMC is committed to a closed model in other markets and competitors would react quickly to rumors rather than waiting for affiliation transactions to close.[5] Penn State was likely slower because it needed Highmark’s financial backing to push forward.[6]

Which specialties are the most special?

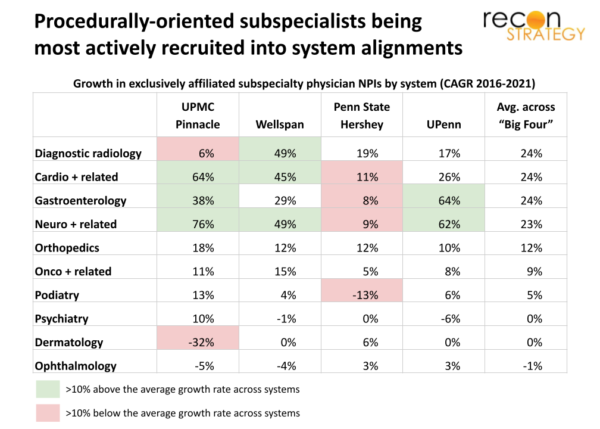

Not all specialties are receiving the same attention. The Big Four already have a large share of aligned physicians in some specialties so may not need many more. For the others, however, different levels of attention likely reflect how the Big Four valued the strategic importance of each specialty. The pattern of attention, therefore, may reveal something about strategy.

Generally, the slowest growth in alignments has been in primary care. While each system already had a good share of primary care in alignments in 2015, overall growth has not kept pace with either facilities-related specialties and specialists since. This suggests the Big Four systems are less focused on expanding their primary care platforms which are essential for the value-based management of large patient populations (but less directly helpful in securing procedural referrals).

Among subspecialties tightly linked with facilities care, growth has been faster than primary care. All of the Big Four largely had anesthesiology and pathology already locked in. However, WellSpan and Penn State Hershey were more reliant on independent hospitalists and emergency physicians in 2015 and concentrated their recruiting and affiliation efforts there while UPMC Pinnacle filled out its general surgery team. Making sure a large share of your key facilities-related physicians are employed can help systems drive consistent clinical approaches to hospital and patient encounters.

The most energy has been spent on alignments in procedural and surgical subspecialties.[7] An average of 23% of Capital District physicians in these subspecialties were aligned with the Big Four in 2015 and about 50% were by 2021.

Different systems have focused on different subspecialties:

- WellSpan invested much more heavily in diagnostic radiology than the other systems (and UPMC Pinnacle seems so far comfortable with non-exclusive providers).

- UPMC Pinnacle, WellSpan and UPenn appear to be in an arms race in neuro, cardiac and gastro, while Penn State Hershey—with historically the largest footprint of aligned physicians—has so far failed to keep pace and saw its leadership position eroded.[8]

- All four systems are building out their teams in orthopedics and oncology.

- Other potentially profitable procedurally oriented subspecialties—such as podiatry, dermatology, and ophthalmology—have so far seen less overall increase in alignments and more share swapping across the Big Four.

Taking ground with clinic expansions

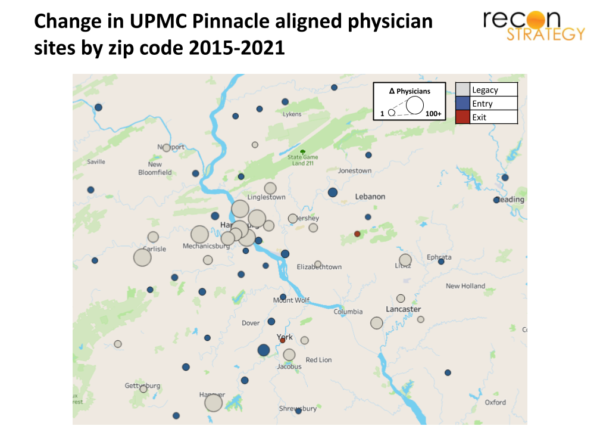

Changes in physician alignments will drive changes in site networks. Physicians aligning with one system can often bring sites of care (e.g. clinics) with them. Systems can choose to retain these sites, consolidate the newly affiliated physicians in other existing locations or build new sites altogether. Systems may also encourage aligned providers to offer care at other legacy locations within their system (e.g., circuit riding). Generally, the outcome is to grow the network to make it easier for patients to seek care.

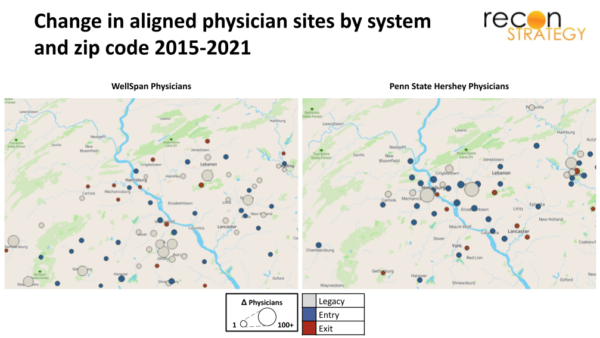

The Capital District is no exception. The map below shows the array of locations where UPMC Pinnacle had aligned providers situated in 2015 (gray), where they obtained new locations for aligned providers to practice (many dots in blue) and where they either lost or closed locations with exclusively aligned providers (fewer dots in red).

The general pattern is an expansion of concentric satellites around the Harrisburg, Carlisle, Hanover and York hubs.

WellSpan and Penn State Hershey have likewise seen an expansion of aligned clinics and sites of care although here the pattern suggests some degree of cooperation:

- Penn State Hershey has been building out around Harrisburg but pulling back to some degree from the WellSpan strongholds to the south (with site closures shown as red dots around Lancaster, York and Gettysburg).

- WellSpan has been growing in the south along the Gettysburg–York–Ephrata axis and “ceding” sites in the north near Penn State Hershey (again, closures shown in red dots).

Several clear zones of contention are emerging in the Capital District:

- UPMC Pinnacle vs. Penn State Hershey in greater Harrisburg

- UPMC Pinnacle vs. WellSpan in Hanover and, to a lesser extent, York

- WellSpan vs. UPenn in Lebanon, Ephrata and New Holland, and Penn State Hershey vs. UPenn in Lititz

Implications

The transformation of the Capital District market from open to closed physician affiliation model is only in midstream and slowed the last year and a half given the pandemic. However, it is possible to draw a few initial learnings from this case study:

Because a competitor getting a head start on building closed model physician affiliations can be so threatening, markets can change very quickly. Systems which have the capital to wage an affiliation campaign will do so, those that lack the resources will find partners (e.g., Penn State Hershey and Highmark).

Because physicians will tend to direct care to the facilities with which they are aligned, the land grab initially tends to focus on procedurally focused specialists rather than primary care. This approach reflects the pragmatic reality of how systems make money today but also suggests these systems’ strategists do not expect population health to be a critical source of economics in the near to medium term.

As systems try to lock in referral flows via aligned physicians, they will lose the opportunity to treat patients from non-aligned physicians. Accordingly, each system will need to expand the presence of aligned physicians geographically to secure patient flow. More geographies will become zones of contention with more systems putting their own aligned specialists in each market. This may create more choice for patients (as long as narrow network benefit designs and ACO networks don’t get in the way) but also potentially add cost from duplication. Hopefully, the savings from each system operating with greater internal consistency and efficiency will outweigh the costs of duplication. Hopefully.

Jacob Wiesenthal

Associate Consultant

Tory Wolff

Managing Partner

To read more about the evolution of UPMC’s economics from 2016 to 2021, download the full report below:

Evolution of UPMC Economics 2016 – 2021.pdf

[1] For this analysis, we compare annual snapshots from Physician Compare, a CMS dataset in which providers report, among other things, their specialty/subspecialty, addresses at which they practice and their hospital affiliations. Updates to Physician Compare depend on physician self-reporting which can be delayed. Therefore, the statistics provided here should be interpreted as directionally correct with a reasonable degree of precision.

[2] We define a physician’s system affiliation based on their hospital affiliations listed in the CMS Physician Compare dataset. A physician can have between zero and five hospital affiliations, described as any hospitals at which the physician provides services. Physicians reported as only providing services at hospitals owned by a single system are classified as exclusively affiliated or “aligned” with that system, while physicians reported as providing services at multiple hospitals owned by different systems are classified as non-exclusive or “non-aligned,” as are any physicians with no hospital affiliations.

[3] Our analysis looks at systems based on their current hospital footprints. Therefore, data comparing physician affiliations include antecedent hospitals that were subsequently acquired by one of the three systems. For example, Summit was acquired by WellSpan in 2018, but physicians affiliated with Summit prior to 2018 are included in the WellSpan data. This approach avoids changes in physician affiliations being passive artifacts of acquisitions rather than initiatives proactively undertaken by the provider system.

[4] In prior research and articles, we have focused on three systems when analyzing the Capital District: UPMC Pinnacle, WellSpan and Penn State Hershey. For this piece, we have included UPenn in the analysis to describe the dynamics of physician affiliations more completely.

[5] Given UPMC Pinnacle’s lower starting share of exclusively affiliated physicians in 2016, its growth between 2016 and 2017 would also have seemed much more aggressive to its competitors.

[6] See The UPMC/Highmark brawl spills into Philadelphia’s backyard – what happens next?

[7] One caveat as well: Both UPMC and UPenn can be filling out their subspecialty capabilities via “circuit riding” specialists from their Pittsburgh and Philadelphia motherships. These physicians could not be captured in the data. These would also likely be more stop-gap solutions until there is sufficient volume to support a new hire in the Capital District.

[8] In fact, by 2021, WellSpan appears to have assembled the largest system-aligned gastroenterology team in the region with 26 aligned physicians vs. Penn State’s 16 physicians.